Illinois in Decline: What Do the Numbers Say?

On Tuesday, August 1, 2023, Greg Bishop of WMAY Springfield's Morning News interviewed me.

We discussed the recently unveiled budget summary for FY2024 by the Illinois Commission on Government Forecasting and Accountability (COGFA). This is a bi-partisan Commission which includes Democratic and Republican state senators and house members.

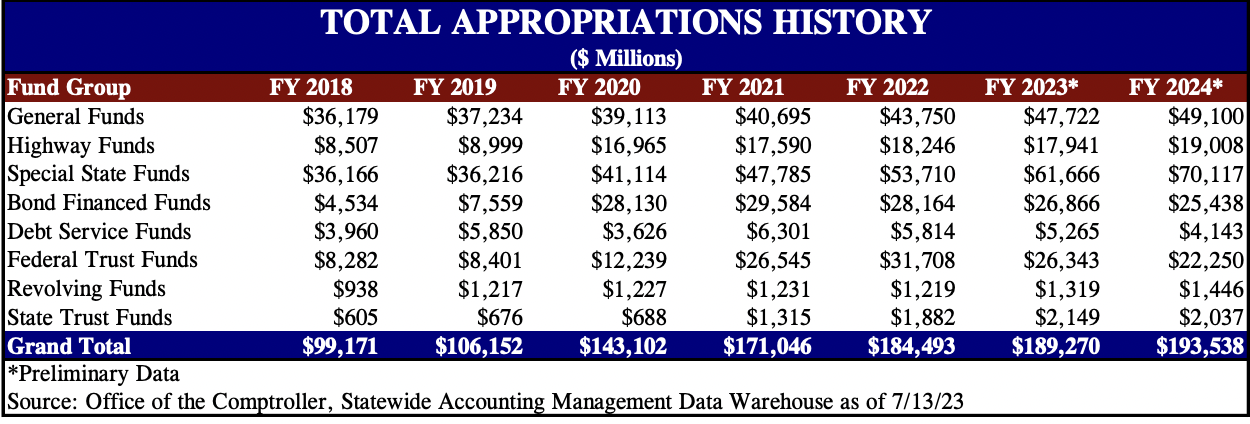

Based upon the schedule included in the report (image below), there was an increase in total appropriations from $99 billion for fiscal year (FY) 2018 to $193.5 billion for FY 2024. Mr. Bishop highlighted for his viewers that appropriations are taxpayer dollars from the federal, state, and local governments. So, even if you aren't an Illinois resident, these are your federal tax dollars.

The most significant increases came during the COVID crisis, with a total appropriations increase of 35% in FY 2020 and 19% in FY2021. Once the crisis was over, appropriations should have returned to pre-COVID levels. Instead, they continue to rise. According to my calculations, if appropriations had continued to increase at a 7% rate, as they did from FY2018 to FY2019, then the estimated FY2024 total would be $149 billion, $44.5 billion less than the $193.5 billion estimated by COGFA.

The budget number mentioned by Governor JB Pritzker and the legislature is $50.4 billion, while the COFGA report puts expectations at $193.5 billion for total appropriations.

Why the discrepancy in numbers? Greg asked.

And this is where the confusion starts, was my reply. It is so confusing that even if the taxpayers paid attention, they would throw their hands up. As an accountant and someone who looks at Illinois' finances all the time, trying to figure out Illinois' budget numbers is like a dog trying to chase its tail.

The $50.4 billion is the “General Funds” budget. What does “General Funds” mean? Here is the definition I found on page 162 of the COGFA’s FY2024 budget summary.

General Funds - (usually lower-case) refers to the following group of funds, inclusively: the General Revenue Fund, the Education Assistance Fund, the Common School Fund, the General Revenue - Common School Special Account Fund, the Fund for the Advancement of Education, the Commitment to Human Services Fund, and the Budget Stabilization Fund.

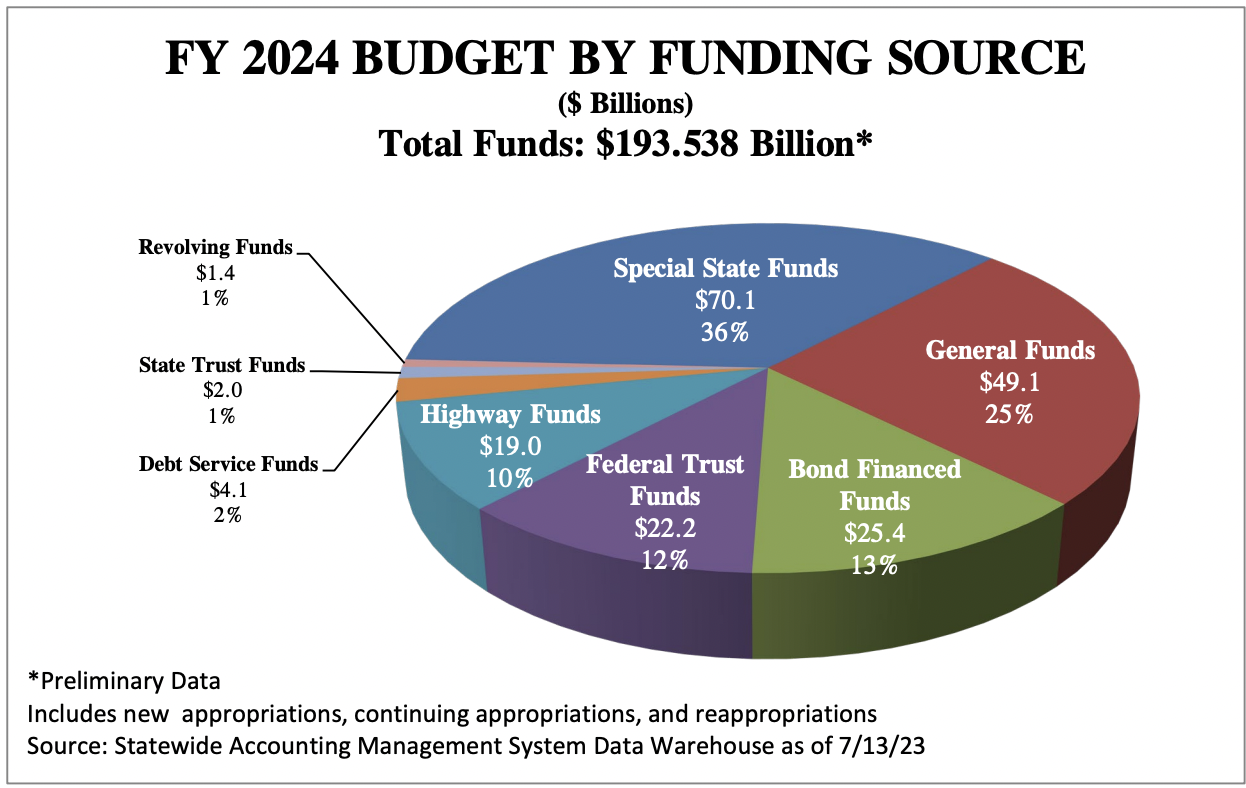

Here is a chart included in the report titled “FY 2024 Budget By Funding Source”:

Now I am starting to get dizzy chasing the numbers. As an accountant, I want numbers to tie together. As Greg mentioned the Governor signed a $50.4 billion budget, but the revenue on the chart above shows the General Funds revenue totals $49.1 billion.

After spending 10 minutes looking at the 177-page COGFA report to find the difference I decided to move on since it’s only a mere $1.3 billion.

Another vital thing to understand is that “Special State Funds” are $70.1 billion, or 36% of all funding sources. In our 2017 Truth in Accounting study, we found Illinois had more than 600 special funds. We concluded that:

Most state governments utilize special funds, which are intended to restrict use of such funds to the specific purpose for which they were created. In Illinois there are more than 600 special state funds listed under Section 5 of the Illinois Finance Act (Illinois Legislative Reference Bureau, 2017) that support activities ranging from cancer research to environmental protection. Some of the large funds include the Local Government Tax, Hospital Provider, State Lottery, and the Road Fund. In many cases special funds are established for a special cause that might not be funded during the normal budget process.

One example of one of the special funds is the "911 Enhancement Fund". I invited his audience to review their cell phone bill for the 911 Enhancement Fee. This special fund is meant to enhance the 911 system throughout the state. For example, when you call 911, it will go to the closest police department. However, the state legislature can sweep this money into the general fund if they decide to use it for other purposes or to balance its budget.

The control and use of Special Funds can be very loosey-goosey. So much so that in 2016 80% of Illinois voters approved the Safe Roads Amendment, which taxes and fees assessed for transportation projects must be used for transportation projects.

At the end of my interview with Greg I stated that we should all agree on two issues.

First, the Illinois budget (or any state or local budget) should not list loan proceeds as revenue. Borrowing to balance the budget is so frequent that page 128 of the COGFA report includes a schedule titled "History of Short-Term Borrowing Act." As noted on this schedule, the budgets were "balanced" for FY2020 and FY2021, while state revenues listed a $3.2 billion loan from the Federal Reserve. (Do you consider your budget balanced if you had to borrow money to pay some bills?)

Second, the state should include its minimum pension contributions when calculating its budget. Unfunded pension benefits are compensation costs that should be accounted for when earned, but instead, they are being charged to future taxpayers' credit cards without making the minimum payment.

In fact, the COGFA report includes a quote from the Fitch rating agency that correctly highlights that the state pension contributions are $4.4 billion short of the minimum payments the state's actuaries say should be contributed to the pension plans. Another chart titled "Change in Unfunded Liabilities" highlights that $58.5 billion of the increase in Illinois' unfunded pension liabilities comes from the state not contributing the minimum payments to the plans.

Those two changes alone would put Illinois on the track to financial honesty and repair.